You did the work. Now take what’s yours.

The 2 a.m. feedings. Office politics. The care calendars. The grind. Decades of labor—paid and unpaid—and somehow Social Security still shortchanges women.

Let’s be clear: This isn’t a gift. It’s your money. It’s payback for every undervalued hour you’ve ever worked, hustled, or cared for someone else.

The system may be flawed, but it was sparked by a woman who understood fairness.

Because—guess what?—the original badass behind Social Security was a woman.

Meet the Woman Who Built Social Security

Frances Perkins, FDR’s trailblazing Secretary of Labor, took charge in the middle of the Great Depression and immediately went to work fixing what was broken, from securing workers’ rights to organize and bargain collectively to pushing for a minimum wage for the most vulnerable. As chair of the Committee on Economic Security, she led the team that built the Social Security Act of 1935, earning her the rightful title of the program’s principal architect. Her grit and vision laid the very foundation of the safety net millions of women depend on today.

“I came to Washington to work for God, FDR, and the millions of forgotten, plain common workingmen.” — Frances Perkins

Perkins was an outlier. The system she helped design wasn’t built for today’s working woman. Now, 90 years later, Social Security is available to women in a variety of situations, but it’s not easy to understand. One example: In a 2025 AARP survey, only 24 percent got the max-benefit age right.

Perkins lit the torch.

Let’s finish the job and unf*ck the confusion.

The 5 Numbers Every Woman Needs to Know

Want to outsmart the system that wasn’t built with your life in mind? Start with these five numbers. Tattoo them to your brain (or at least your Notes app). Because for every one of you who’s left money on the table, these five must-knows are your line of defense.

1. Full Retirement Age (FRA): 66–67

This is when you get 100 percent of your benefit. Prior to 1983, this was 65. Now, your exact FRA depends on the year you were born. Earlier than that? Smaller check. Later? Bigger one.

2. Age 62: The Earliest You Can Claim

Yes, you can start claiming at 62. But don’t get too excited—it’ll only be about 70 percent of your full benefit. It’ll be a smaller check for life, but sometimes survival is more important than strategy.

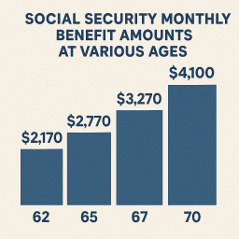

3. Age 70: The Max-Out Moment

Wait until 70 and your check jumps to 124 percent—8 percent more for every year after FRA. This is Social Security saying, “Fine, you win.” And hell yes, you do.

4. 10 Years of Work

That’s the minimum number of years you need to work and pay into the system to qualify for benefits. Less than that? No check. Just rage.

5. 35 Highest-Earning Years

Your benefit is based on your 35 best years of income. If you took time off (for caregiving, motherhood, life), those years count as $0—and they drag down your average. Oof.

PRO TIP: Freelance or part-time work now can replace those $0s—and boost your payout.

The Power Move: When to Claim (and When to Wait)

Your Social Security check isn’t just a number—it’s a power move.

“Every year you delay claiming it after full retirement age, your benefit grows by about 8 percent,” said Cary Carbonaro, a Certified Financial Planner (CFP) and author of Women and Wealth. That’s up to 24 percent more if you wait until age 70. Not bad for doing literally nothing but waiting.

Cassandra Kirby, a CFP and CPA, shared a typical example:

Real talk: Delaying payments could mean hundreds or thousands more per month—for the rest of your life, said Kirby. Multiply that by a couple of decades, and we’re talking serious money. Like “move-to-Portugal” money.

But what if 62 feels like salvation and your job’s killing your soul? What if you’ve buried too many friends and family to believe you’ll even make it to 80?

Claiming early might be the smartest move if you’re strapped for cash, dealing with health issues, or your family tree doesn’t exactly scream “longevity.”

PSA: You’ve got options:

- Changed your mind? You can withdraw your claim within 12 months and reapply later—but you’ll have to pay back what you already received.

- Past FRA? You can pause benefits once and let them grow until 70.

So yes, the math says “wait if you can.”

But your life—your energy, your health, your happiness—matters just as much.

Whether you left him, lost him, or ran the damn household while he played fantasy football, Social Security still owes you. If you were married and your paperwork is in order, there’s likely a check with your name on it. Don’t let bureaucracy deny you.

Divorced, Widowed, or Out of the Workforce?

Married 10+ years, now 62+ and single? You can claim up to 50 percent of your ex’s benefit—even if he hasn’t filed, said Carbonaro. As long as you’ve been divorced at least two years, you don’t need his permission or even a heads-up. There’s no bonus for waiting past full retirement age, so file when it works for you. Just one rule: no double-dipping. If your own benefit’s higher, take it and don’t look back.

Lost your partner? You can claim survivor benefits as early as 60—no need to wait, said Kirby. That gets you 71–99 percent of their benefit; wait until full retirement age, and you get the full 100 percent. Married at least nine months? You’re in.

PRO TIP: Start with survivor benefits, then switch to your own at 70 if it’ll be higher. That 24 percent boost? It adds up.

Didn’t work full time because you were raising humans, wrangling schedules, and holding the damn fort? Social Security still owes you. If you’ve been married at least one year and your spouse is collecting, you can claim spousal benefits. Wait until full retirement age, and you’ll get up to 50 percent of your check. Claim early, and it drops to about 32.5 percent. Delaying past full retirement age won’t increase it—so don’t bother.

Still Working? Don’t Leave Money On the Table.

You’re still clocking in because you love it or need it. But if you’re collecting Social Security before full retirement age, the system is set up to quietly shave dollars off your check. Rude.

Earn over $23,400, and Social Security claws back $1 for every $2 you make.

Plus, if your “combined income” tops $25K (single) or $32K (joint), up to 85 percent of your benefits can get taxed. Combined income = wages + investments + half your Social Security.

Bottom line: Working is great, but know the thresholds. Otherwise, the IRS gets the raise—not you.

You Built This. Don’t Leave a Dime Behind.

Every dollar, every law, every bit of progress owes you. Don’t wait—claim it, share what you learn, and help another woman do the same. You’ve earned it, and the revolution starts wherever you cash that first check.

******

FINANCIAL DISCLAIMER

The information provided on PROVOKED is for general informational purposes only and does not constitute financial, legal, tax, or investment advice. SFD Media LLC and its contributors are not licensed financial advisors, investment advisors, brokers, accountants, or attorneys. You should consult with a qualified professional before making any financial decisions based on this content. While efforts are made to ensure the accuracy and timeliness of the information, SFD Media LLC makes no representations or warranties, express or implied, regarding its completeness, accuracy, or applicability to your individual circumstances. Reliance on any information from this site is solely at your own risk and discretion.

3 Responses

I’ve been reading a lot about this lately. The biggest take away is that social security wasn’t designed to make us wealthy, it was designed to “make us wait.” It almost evens out by taking it at 62 vs 70 because theoretically, we’re living longer to enjoy it. If taking it early is viable, it can be also be invested in high interest savings, etc. Definitely worth considering all the options.